Executive Summary

Redfin (redfin.com) is a technology-enabled brokerage providing on-demand solutions for the $75 billion residential real estate market. The company operates in over 80 markets and increased revenue 46% annually from 2014 to 2016. Similar to other local marketplaces (e.g., ride sharing), Redfin utilizes a technology backend to enable go-to-market strategies in each of the markets it enters. The hybrid “human + technology” model is a key component to its differentiation in a very competitive real-estate market. As Redfin enters a new phase of growth post-IPO, Redfin will potentially be focused on its path to profitability as well as its ability to efficiently scale in additional markets. Redfin’s competition comes in the form of traditional brokerages pursuing a technology driven approach as well as upstarts that are trying to follow in Redfin’s footsteps.

Tech-Powered Real Estate.

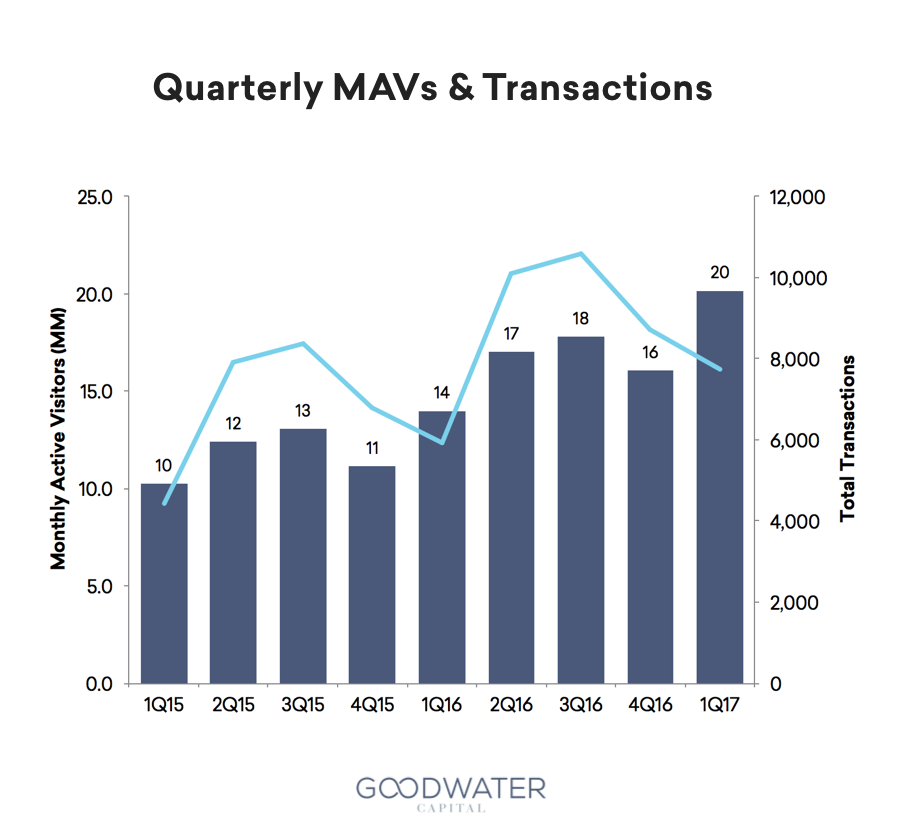

Founded in 2002, Redfin’s mission is to redefine real estate in the consumer’s favor. The company has created tools that enable both its customers and agents to make the buying and selling of residential real estate more efficient and affordable. With headquarters located in Seattle and agents in over 80 markets, Redfin has leveraged its technology and improved the real estate transaction experience to bring 20 million Monthly Average Visitors (“MAV”) and 935 lead agents to its platform as of Q1 2017.

The Market Opportunity.

The US residential real estate market is large with over $75 billion in commissions paid through 5.5 million total home sales in 20161. The industry is highly fragmented with Realogy (the largest offline owner of US residential real estate brokerage offices including brands like Century 21, Coldwell Banker, and Sotheby’s) serving 6% of this $75 billion market. Redfin currently serves only 0.6% of the market.2

Winning Strategies

What can entrepreneurs and investors learn from Redfin’s path to IPO?

- Focus on the end customer: Redfin’s mission is clear – to save consumers money and time while providing an enjoyable experience. Their NPS (net promoter score) of 50 reflects the company’s consumer-centric focus3. Home sellers save up to 1.5% on commissions while buyers receive an average of $3,500 in the form of refunds/rebates. In addition, Redfin is moving towards an on-demand experience where 47% of tours are now scheduled automatically through the app/website. Finally, by directly employing agents versus using contractors as many traditional brokerages do, Redfin can set a higher bar for customer satisfaction.

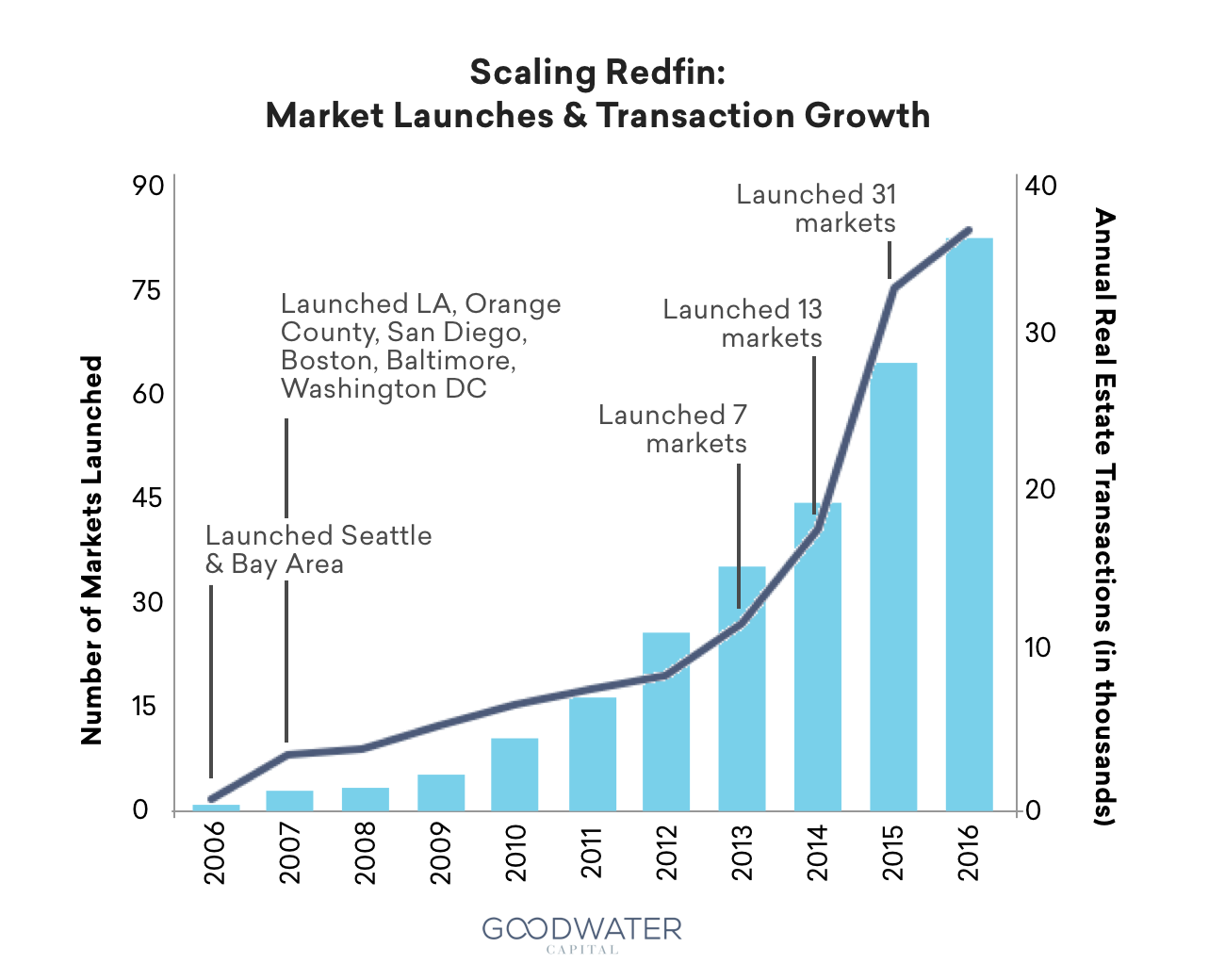

- Patience is a virtue: Redfin was founded in 2002 and will go public just prior to its 15-year anniversary. The company first hired a lead agent in 2006 and aired it first TV commercial 12 years after it was founded. In an age where startups are often pushed towards overnight success or “momentum,” Redfin is a good reminder that to disrupt an institutionalized industry like real-estate, it can take years, or decades, but can be worth the wait.

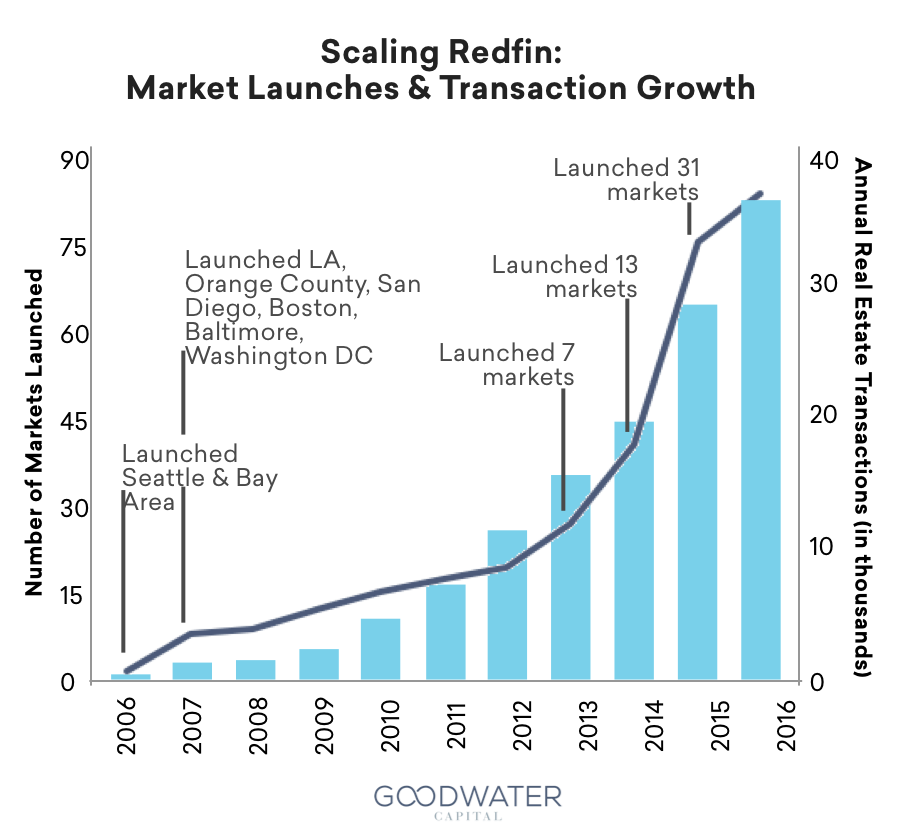

- Smart growth driven by observed market demand: To strike the right balance of supply and demand in each of its markets, we can infer that Redfin stages the level of services it provides based on demand signals. This is critical to avoid the common mistake of over-investing in markets before achieving product-market fit. Before hiring lead agents, Redfin will first observe leading indicators such as web traffic in a certain market to determine if demand has reached a sufficient level to justify investing in agents. Redfin also utilizes its partner network to backfill capacity before bringing on additional Redfin agents to keep utilization high. Additional services such as Redfin Mortgage (loan origination for home buyers) and Redfin Now (Redfin buys the homes upfront from sellers and then sell to buyers) are also driven by data signals and are rolled out to markets that show a propensity to those products. This allows Redfin to make sure the unit economics and profit margins of each market cohort continues to improve, making better allocations of capital investment when needed.

The Next Level

How does Redfin continue its path toward market leadership?

- Outpace the competition on customer value: With both incumbents as well as startups pursuing a “technology first” approach in real estate, Redfin will continue to face competition from all sides. In addition to technology becoming more ubiquitous, competitors such as Zillow and OpenDoor are moving even further towards vertical integration with products such as Rocket Mortgage and OpenDoor’s core service of buying homes directly from sellers. To keep up with this competition, Redfin will need to continually improve its product offerings through initiatives such as Redfin Now and Redfin Mortgage.

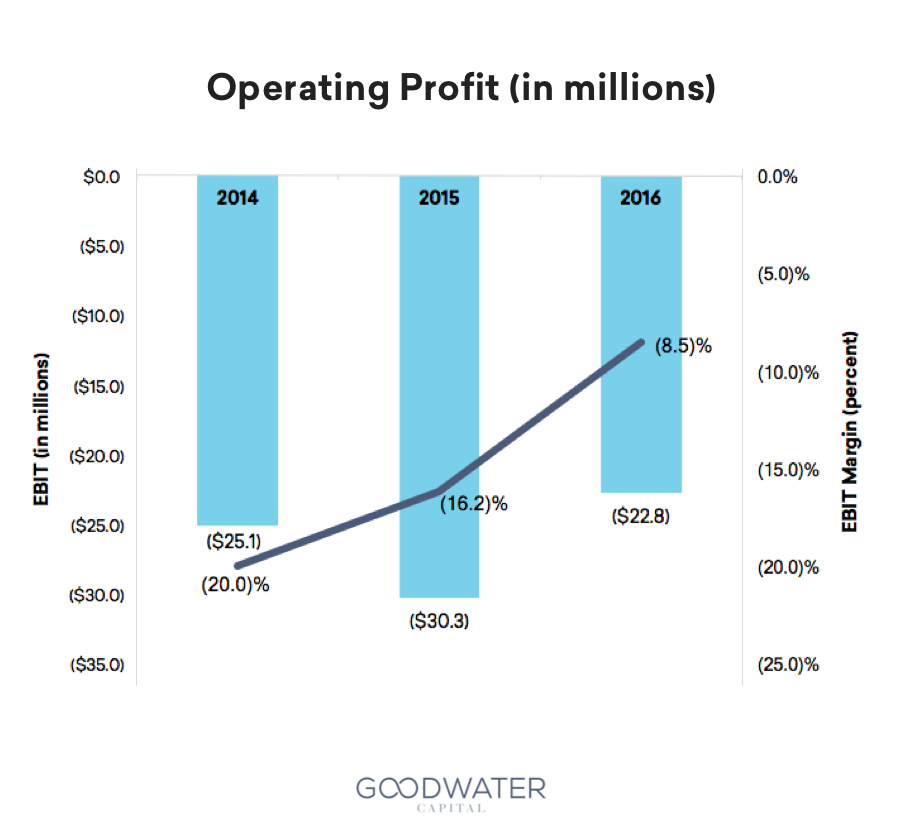

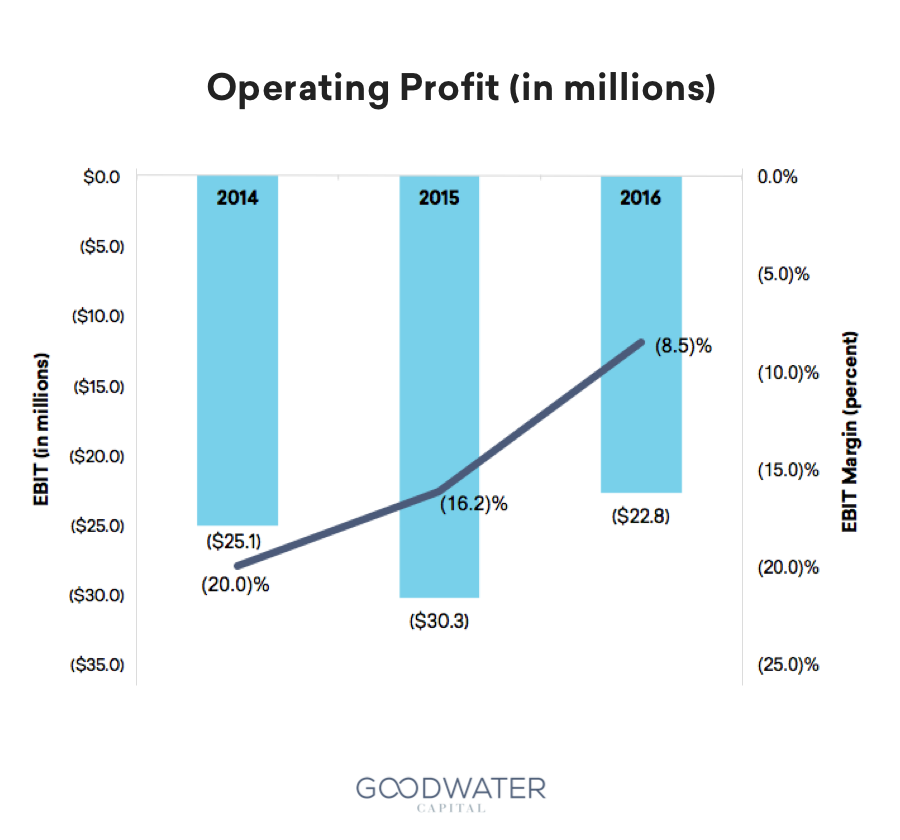

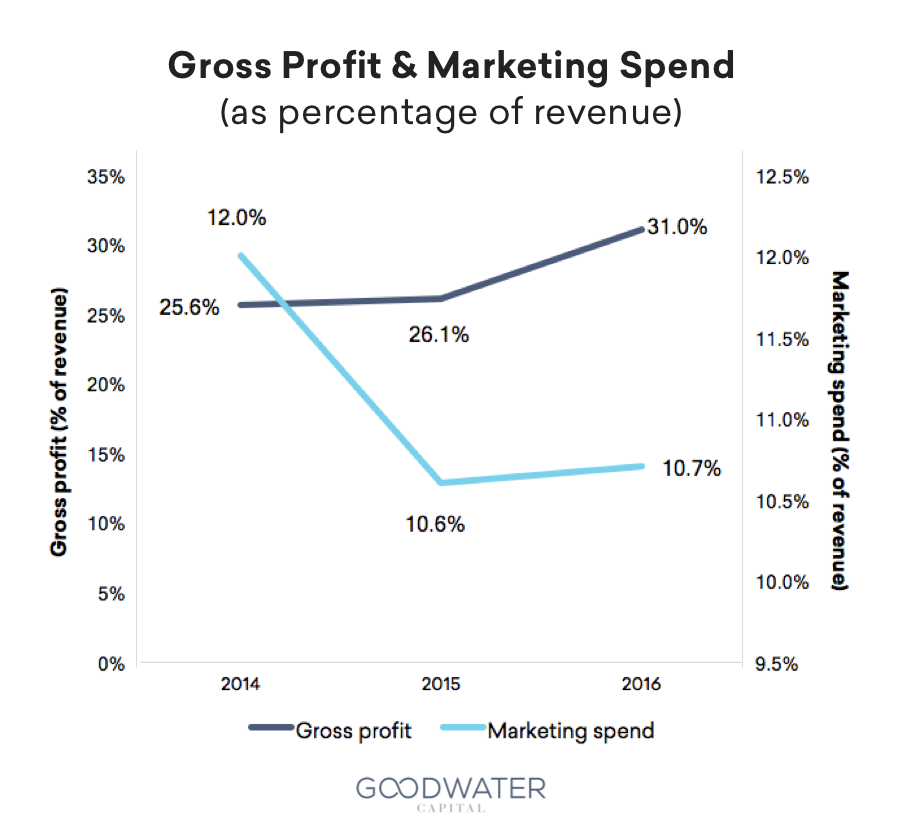

- Demonstrate a clear path to profitability: Redfin remains unprofitable with operating losses of $23M in 2016. The company has demonstrated improvements in gross margin (25% to 31% from 2014 to 2016) and efficiency in marketing spend (12.7% to 10.6% from 2014 to 2016), which will help position the Company to chart a path to operating profit. That said, Redfin’s model is sensitive to the utilization of the agents that it employs directly. How it manages this utilization at scale will be a key component to its continued march towards profitability.

- Increase penetration of existing markets: Though Redfin has gained share in 55 markets since 2014, it will need to drive further penetration in all 80 markets and open new ones as well. Scale does matter and each local market Redfin expands to has nuances that could impact the efficiency of Redfin’s marketing spend. Initiatives such as Redfin’s centralized transaction center in Chicago could help provide Redfin economies of scale and service advantages as it opens new markets.

Market Landscape

Real estate is an industry ripe for disruption. Over one-third of middle-class consumer spending is on the home. With an aggregate of $1.5 trillion spent on US home sales across 5.5 million total transactions in 2016, consumers paid more than $75 billion in commissions.4

Besides residential brokerage firms, the real estate industry encompasses a wide variety of companies and services, including property and lease management (e.g. Cozy and Mynd), short term rentals (e.g. Airbnb and Pillow), commercial real estate (e.g. Costar and Ten-X), subletting and leasing solutions (e.g. Flip and Joinery), and mortgage technology for better home loan experiences (e.g. Blend Labs and Roostify).

Below is a summary of businesses focused on residential real estate transactions in the United States. In addition to the traditional real estate brokerage companies, new firms have arrived leveraging technology to improve the traditional brokerage model ranging from businesses improving single parts of the experience to owning the real estate transaction experience from start to finish.

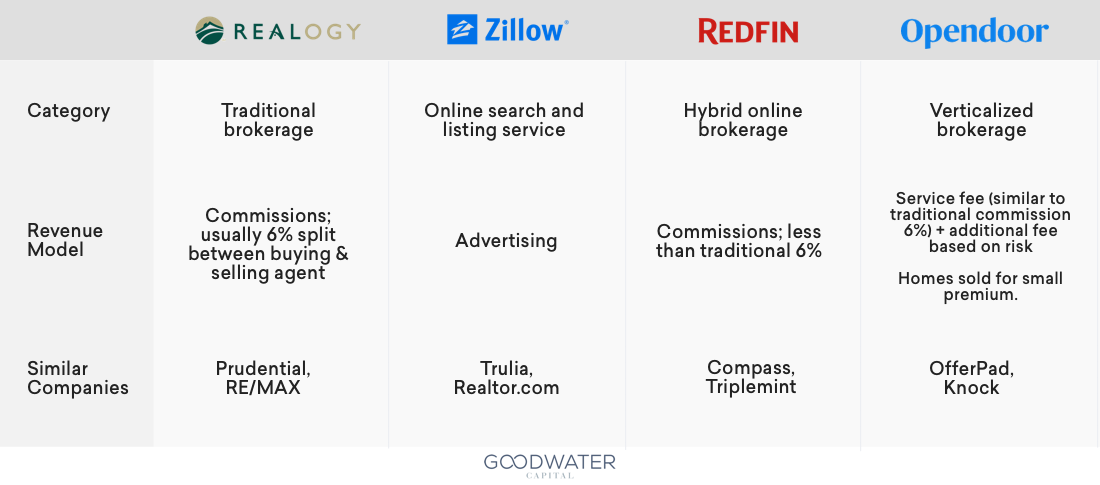

- Traditional brokerages have deep knowledge of the real estate industry, strong local branding, broadly distributed networks of agents within each market, and processes to help consumers through the real estate transaction. As the incumbents, major players include familiar brands such as RE/MAX, Prudential Real Estate, and Realogy, which own or partner with notable entities like Coldwell Banker, Sotheby’s, Century 21, and The Corcoran Group. While these businesses largely operate offline, technology-enabled competitors have pushed these giants to adopt technology into their operations and services. For example, traditional brokerages started publishing MLS information on their websites in the mid-2000s as a direct response to hybrid brokerages doing the same. Noteworthy, most traditional brokerages do not employ agents directly, but work with agents on a contract basis. This is a key point of comparison to the Redfin model that employs agents directly.

- Listing and search services aggregate home listings to provide users with free detailed information on properties, which transformed an industry where knowledge was previously concentrated among real estate brokers. Listing and search services such as Zillow, Trulia (owned by Zillow), Realtor.com (owned by News Corp), and Estately (strategic investment from Realogy) provide home listing information in addition to contextual data, but do not shepherd consumers through the transaction process. Their business models are largely based on ad revenue, where real estate agents pay for ad impressions that are delivered to users in specific zip codes to drive lead generation. Zillow, a more mature player in the space, is primarily a listing and search service, but has also expanded into related areas like mortgages and apartment rentals.

- Hybrid online brokerages are technology-enabled brokerages that systematically leverage technology to add value for consumers by increasing efficiency, providing transparency, and reducing commissions. Redfin was a pioneer in establishing this next generation real estate brokerage model, and a number of companies have drawn inspiration such as Triplemint, Compass, Reali, and Open Listings. While all of these companies are next generation tech-enabled brokerages, they vary with respect to commission models, business operations, listing information, and geographic focus. For example, Redfin determines commission based on a formula, Open Listings gives 50% commission back, and Reali keeps only ~$5,000 and gives back the rest to the user. While Redfin employs salaried agents and pays bonuses based on customer satisfaction, Compass hires agents as contractors and bonuses are based solely on commission. Some brokerages base commission on the listing price while others use the actual price.

- Verticalized brokerages are similar to hybrid online brokerages which heavily leverage the efficiency gains of technology, but they also take on inventory and own the purchase experience from start to finish. Verticalized brokerages operate on the assumption that consumers value the certainty of sale offer to consumer, which is not possible in the traditional market. They simplify the home selling process by directly purchasing homes from consumers. These companies make money by taking a service fee similar to real estate commission, plus an additional fee based on transaction risk; they make fixes recommended by inspectors and try to sell homes for a small premium5. A highly disruptive model, verticalized brokerages bring transparency to real estate transactions, from allowing sellers to secure automated offers, to offering price guarantees to buyers, to allowing consumers to transact seamlessly on a single platform. OpenDoor pioneered this space, setting off a trend of following companies that provide a similar service with variations in geography and types of properties. OpenDoor only makes offers in the mid-tier range, while OfferPad buys a broader set of properties; Knock focuses on Atlanta and Amne focuses on Austin.

The real estate space has a broad array of technology services that impact the process of how residential real estate is bought and sold today. These services are complementary to both traditional and online brokerages and will be interesting to watch as the real estate space evolves.

- Chatbots and AI: AI personal assistants can qualify leads as well as manage client questions. By automating a part of real estate and pushing toward the next frontier of customer service, chatbots embody the spirit of real estate technology trends. Notable real estate chatbots include Ask Doss, Holmes, and Riley.

- Media and imaging tools: 3D models and tours of listings facilitate purchase decisions, and allow consumers to make purchase decisions without going to the house. Real estate brokerages are increasingly integrating virtual tours of 3D models and 360 videos of listings. Sotheby’s uses 3D integration, and Matterport does 3D listings for Redfin.

- Sharing economy: Online marketplaces are increasingly democratized and changing how real estate decisions are made. For example, users can buy larger houses and plan to rent out the space on Airbnb. With the ubiquity of ride sharing services like Lyft and Uber, users are more open to purchasing property with no garage.

Redfin Business Overview

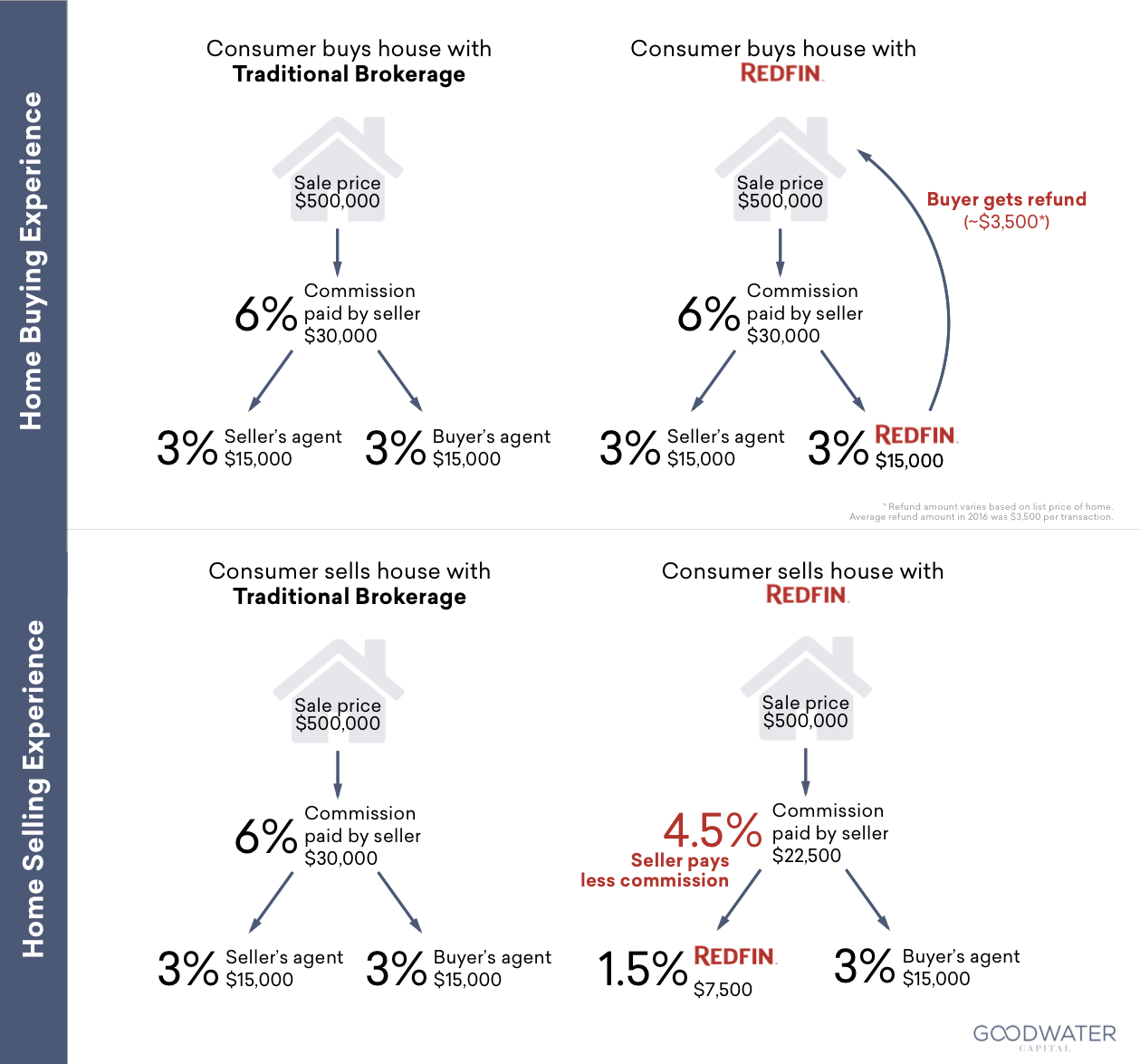

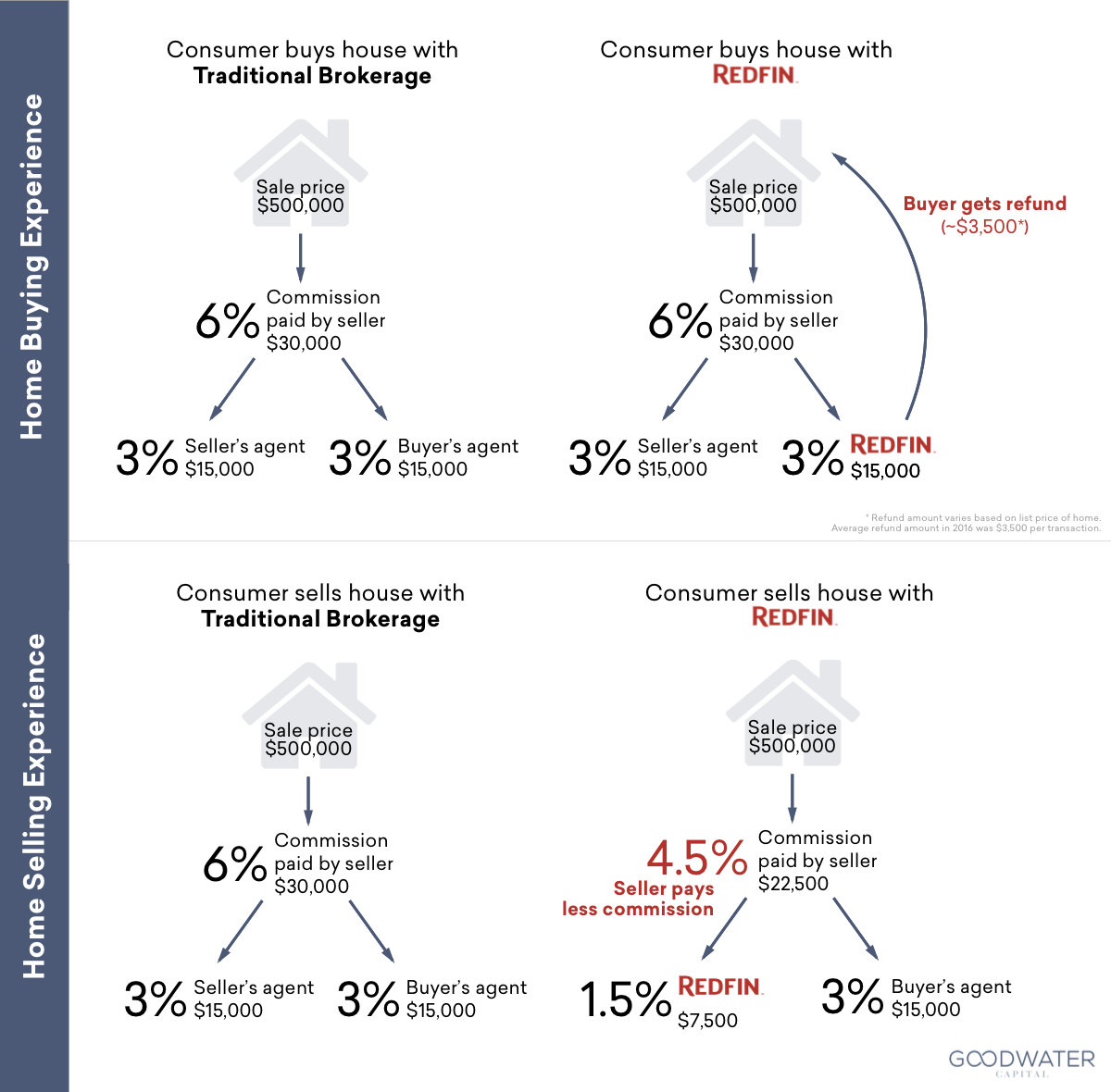

Founded in 2002, Redfin is a technology-powered residential real estate brokerage servicing over 80 markets throughout the US. Its mission is to redefine real estate in the consumer’s favor.6 With headquarters located in Seattle, Redfin’s strategy is to pair its own agents and Redfin’s technology with customers to deliver a service that is faster, better, and costs less. Below is a graphic that describes how Redfin saves both buyers and sellers of homes money in a real estate transaction.

Redfin’s homebuyers saved on average approximately $3,500 per transaction in 2016.7 The company charges most home sellers a commission of 1% to 1.5% compared to the 2.5% to 3% typically charged by traditional brokerages.

Some interesting highlights of Redfin’s business results from its IPO filing are below:

- Helped customers buy or sell more than 75,000 homes worth more than $40 billion through 2016

- Gained market share in 81 of its 84 markets from 2015 to 2016

- Drew more than 20 million monthly average visitors to its website and mobile application in the first quarter of

2017, 44% more than the first quarter of 2016, making Redfin the fastest-growing top-10 real estate website - Earned a Net Promoter Score, a measure of customer satisfaction, that is 32% higher than competing

brokerages’, and a customer repeat rate that is 37% higher than competing brokerages’ - Sold Redfin-listed homes for approximately $3,000 more on average compared to the list price than competing

brokerages’ listings in 2016 - Employed lead agents who, in 2016, were on average three times more productive, and earned on average twice

as much money as agents at competing brokerages; Redfin lead agents were also 44% more likely to stay with the company from 2015 to 2016 than agents at competing brokerages

One of the key advantages of Redfin over some of the new technology companies that have emerged, like Zillow and others, is that Redfin is a brokerage company that has access to multiple listing services (“MLS”) and therefore generally has more updated data than those companies that are not brokerage companies which rely on other ways of getting home listings and historical transaction data. However, the incumbent traditional brokerage companies may have advantages over Redfin and new technology companies in that they may have stronger brand recognition and extensive relationships with participants in the residential real estate industry.8

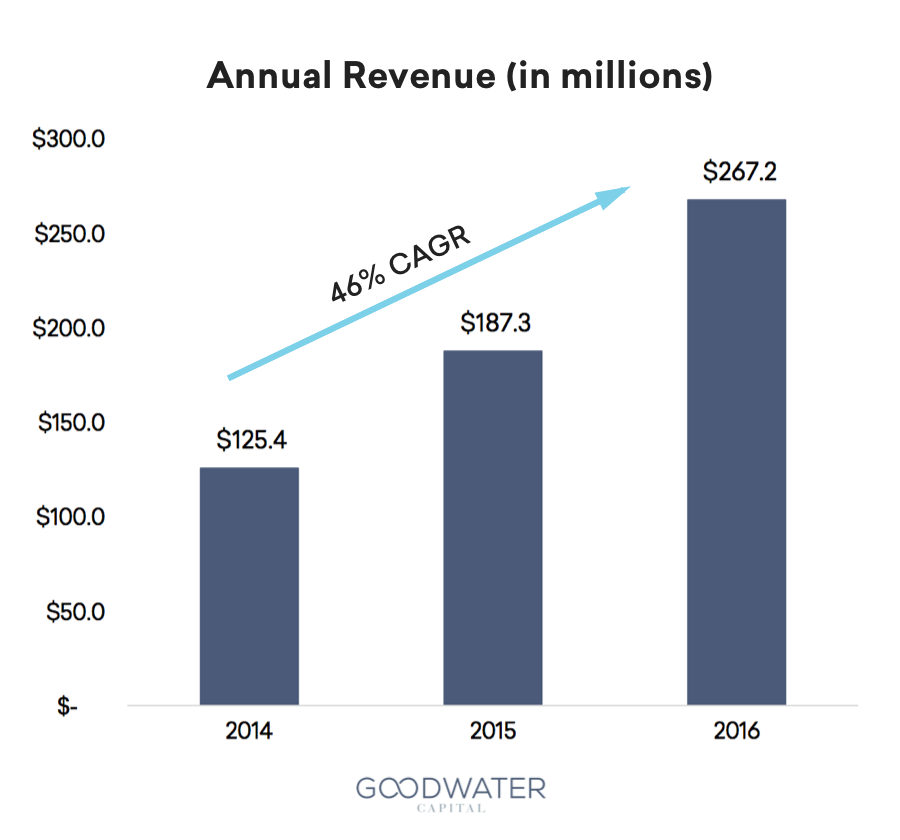

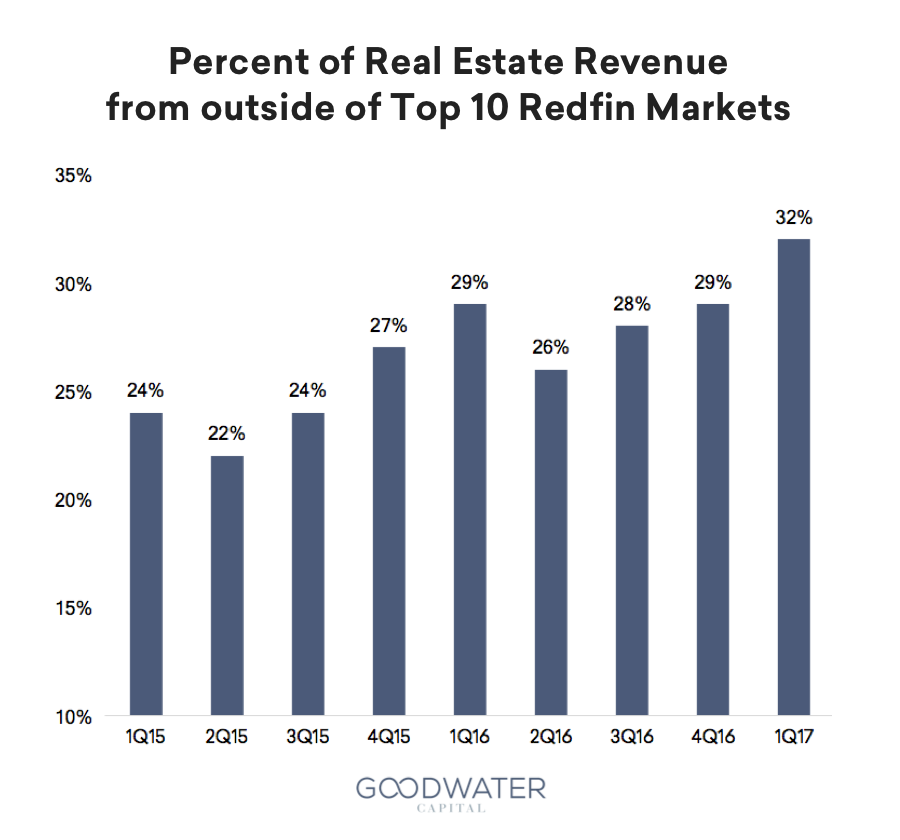

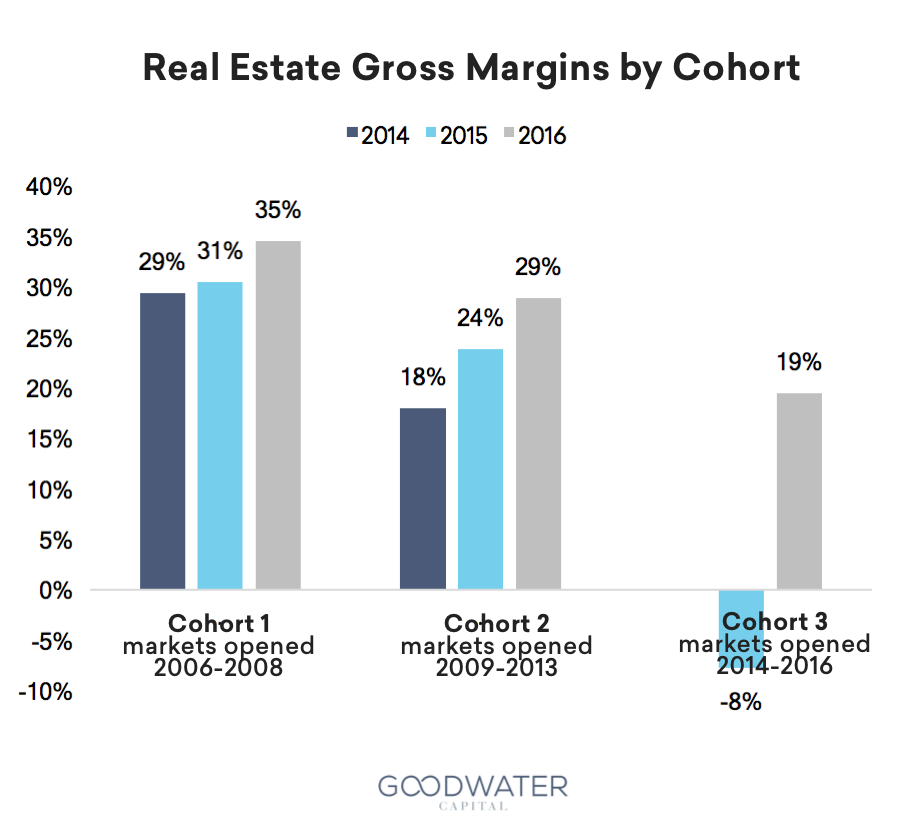

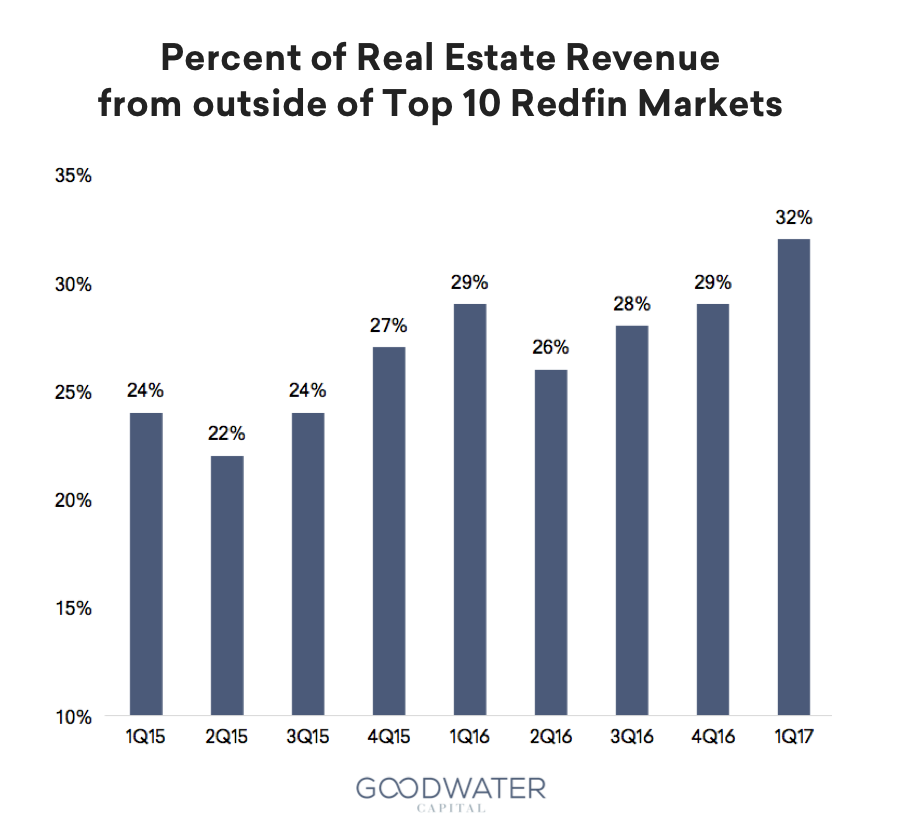

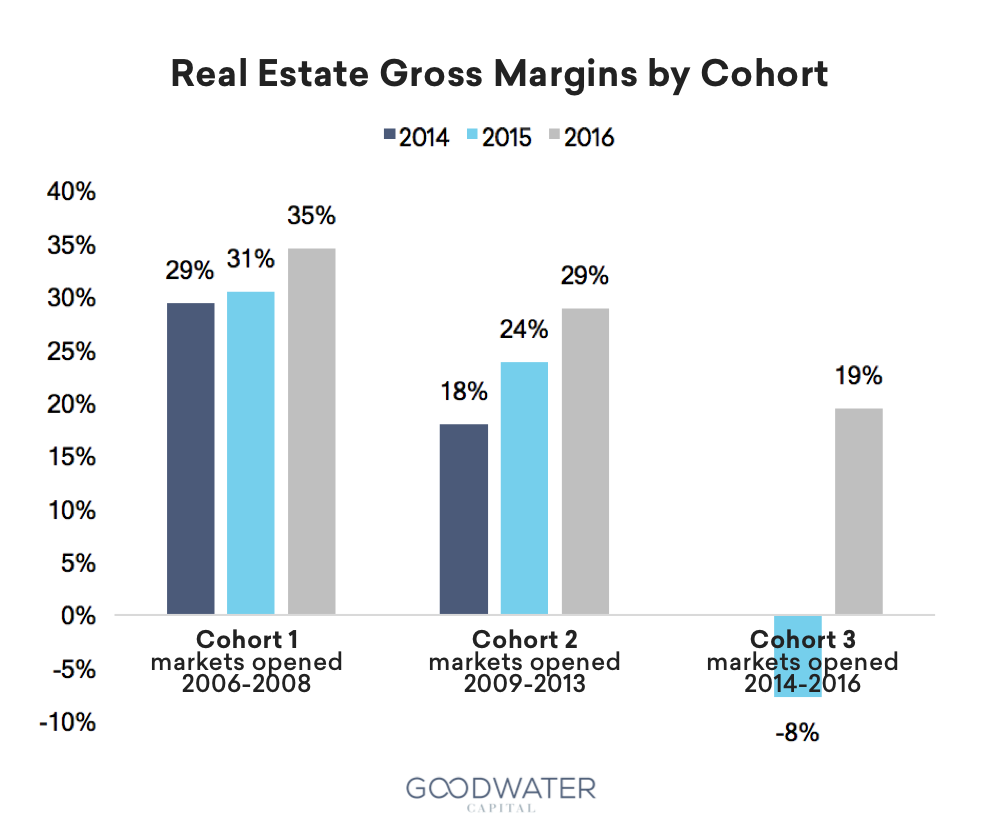

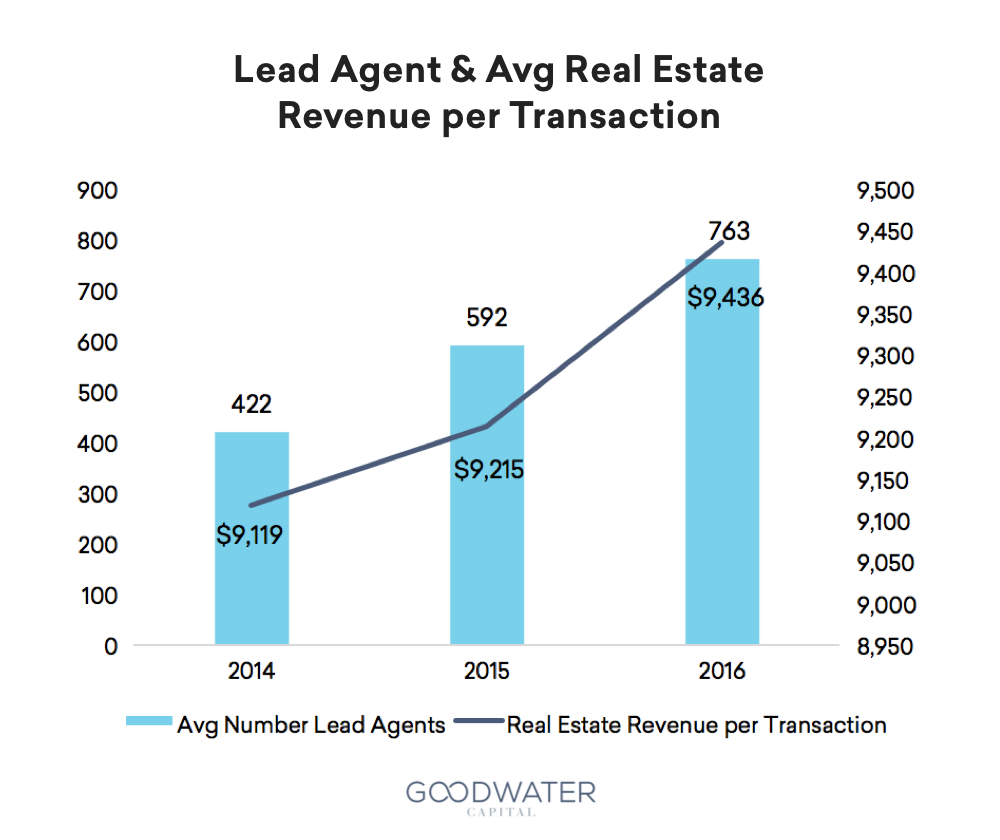

The company has gained market share, increased revenue, increased real estate revenue per brokerage transaction, and increased real estate gross margin in all of the cohorts in each of the years presented. From year-to-year, Redfin’s market share gains have been largely consistent within cohorts.9 As a result, the Company has increased revenue at a compounded annual growth rate of 46% from 2014 to 2016. Additionally, as the Company has successfully entered and gained share in new markets, Redfin has diversified its revenue over time, increasing revenue generated outside of its Top 10 markets from 24 in Q1 2015 to 32% in Q1 2017.

Redfin has experienced gross margin expansion from 25.6% in 2014 to 31.0% in 2016, largely driven by a reduction in personnel costs and improvements in costs associated with home touring and field costs (as a percentage of revenue). The Company has also decreased marketing costs as a percentage of revenue as it continues the markets in which it launched in 2014 continue to mature. These improvements in gross margin and operating costs (as a percentage of revenue) have yielded steady declines in operating losses as a percentage of revenue from 20% in 2014 to 8.5% in 2016, indicating that the Company has experienced operating leverage as markets mature and they achieve greater scale.

Redfin’s first cohort primarily consists of major metropolitan areas, such as Seattle, San Francisco, Los Angeles, Boston, Washington, D.C., and Chicago. The company’s second and third cohorts primarily consist of smaller metropolitan areas, such as Sacramento, Portland, and Raleigh in its second cohort, and Minneapolis, Cincinnati, Nashville, and Kansas City in its third cohort. Redfin believes the continued market share growth trend in its earliest cohort demonstrates possible revenue growth rate and margin trends over time as its newer markets mature.10

Key Risks

There are a number of risk factors to Redfin’s long-term prospects, including:

- The real estate market is a seasonal and cyclical industry impacted by macro and micro economic downturns

- Redfin had negative $26 million in 2016 free cash flow and may not be cash flow positive for many more years.

- The company has significant competition, coming from traditional brokerage companies becoming more tech-enabled and from new “pure” technology companies, including potentially Amazon.

- Redfin may not be able to be as successful in new markets and may earn less in these new markets as the newer markets are generally smaller with lower transaction values.

- The company already sees seasonality in its business, which might indicate a slowing and maturing business.

Goodwater Consumer Research

In Q1 and Q2 2017, we conducted a consumer survey with 6,000 participants in the United States. The panel was representative of census data, balancing age, income, gender, and geography. Survey respondents reported on their usage across a broad range of consumer technology products and services.

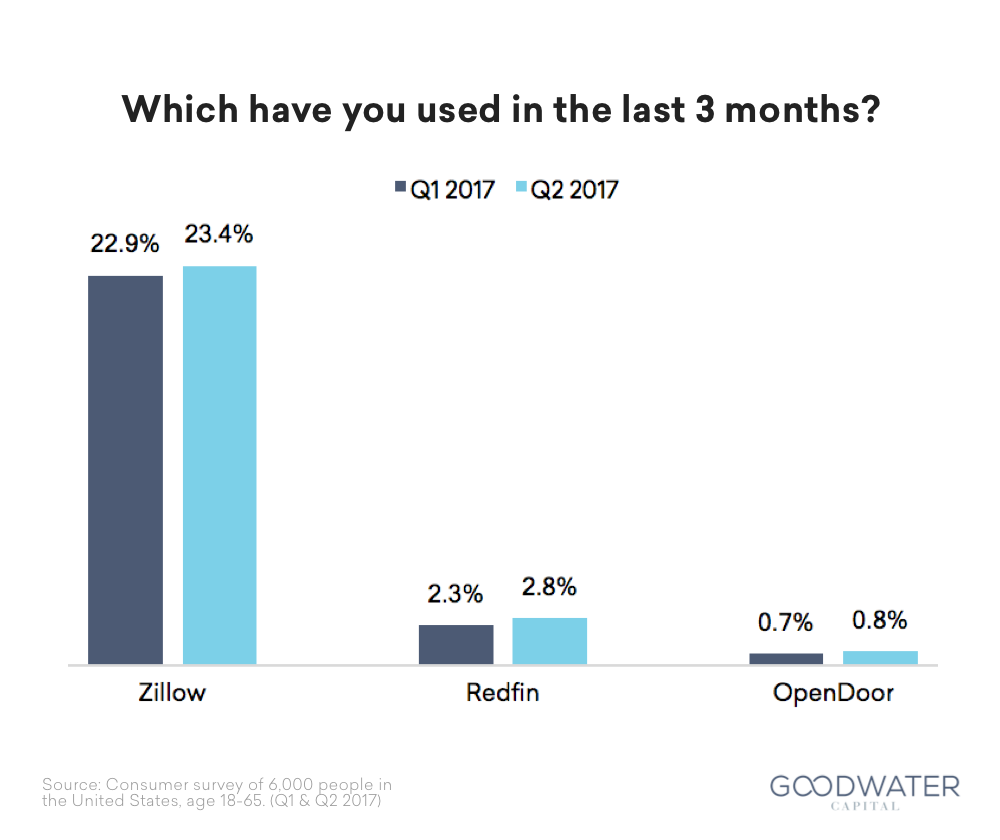

Zillow was the most used online real estate service, where usage refers to interactions with a service (app or website) and does not imply transactions. Twenty-three percent of survey respondents used Zillow and 3% used Redfin; this was consistent across Q1 and Q2 this year. As expected, the demographic of respondents who use online real estate services skew slightly toward older users (over 30 years old) and strongly skew toward more affluent users (over $50,000 annual household income).

Zillow’s dominating usage can be attributed to increased brand awareness because of its maturity in the market. In addition, Redfin and Zillow have drastically different business models with different distribution strategies. Zillow is an online real estate marketing platform, which can expand quickly because it is a software business with services that are relevant to a broad spectrum of users in the real estate space. Zillow’s products appeal to a much larger audience of consumers, both in-market home buyers and existing homeowners. In contrast, Redfin is an online brokerage, which appeals to a narrower audience, and needs to be more deliberate about entering new markets because of additional overhead in setting up offline resources like hiring on the ground agents.

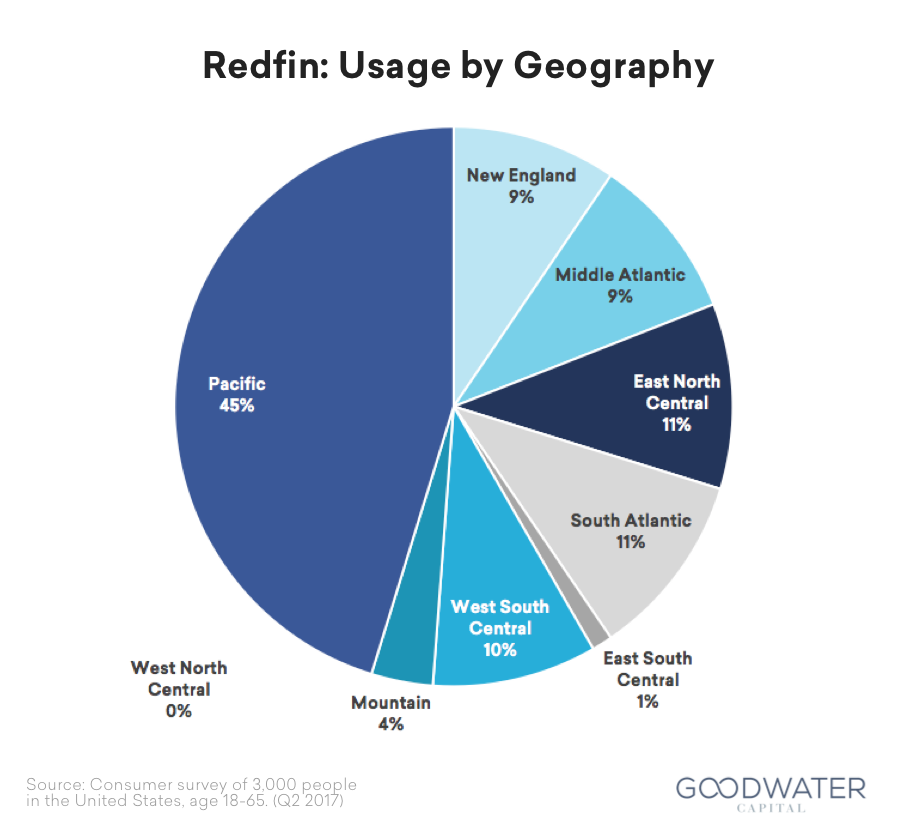

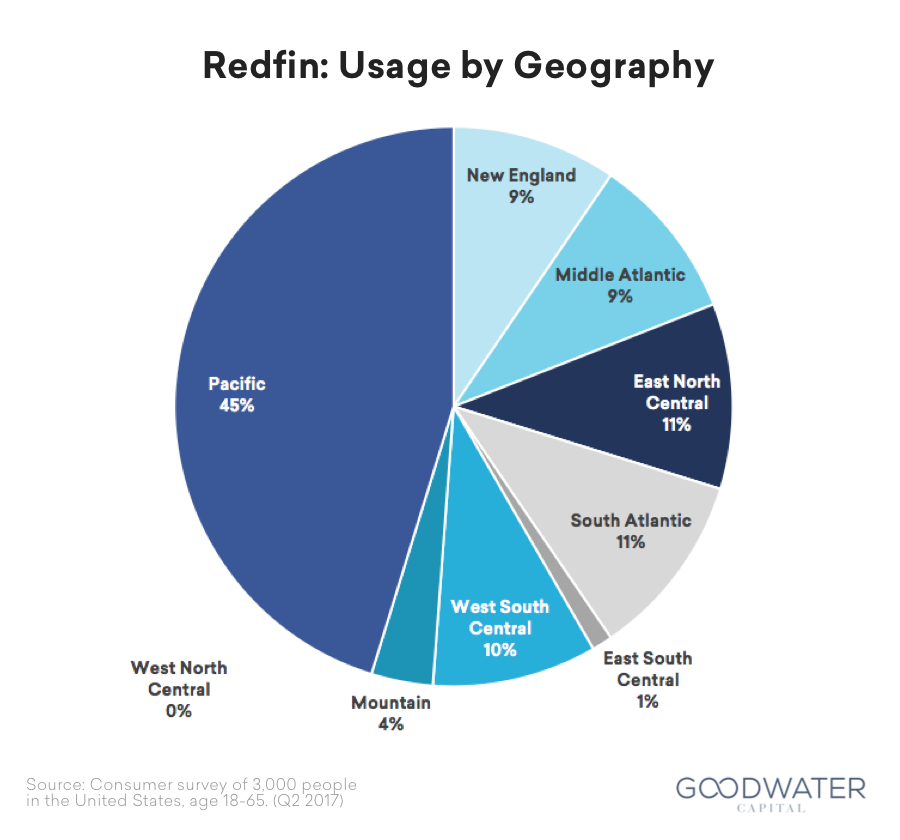

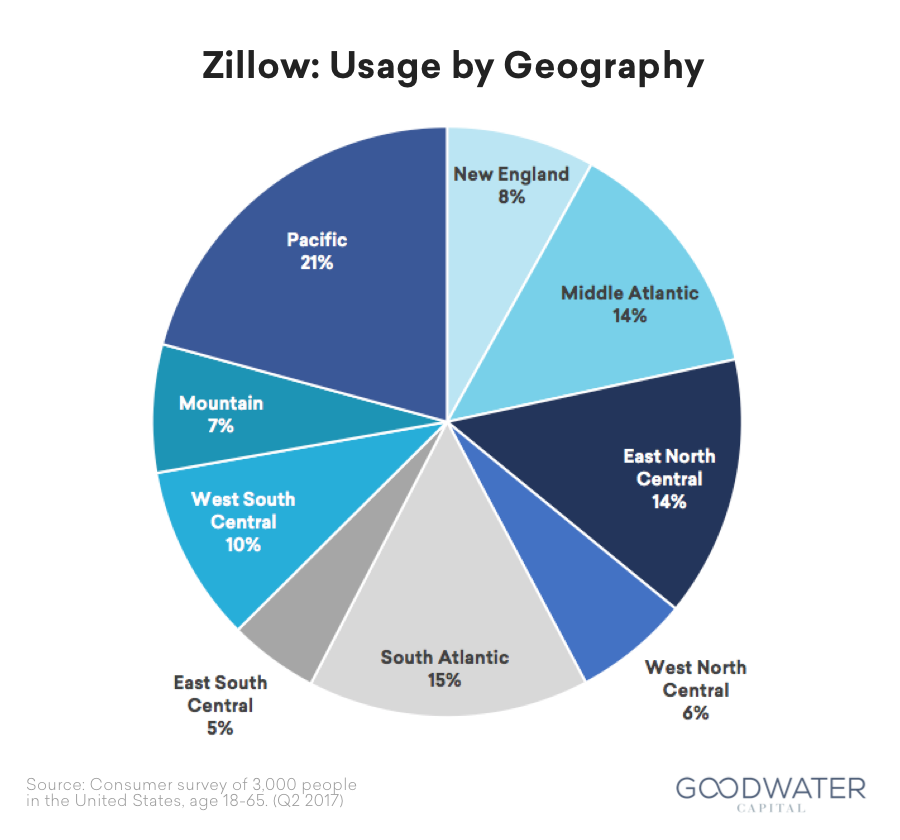

With respect to geography, Redfin usage is largely concentrated in the Pacific region while Zillow is evenly distributed across the United States. Forty-five percent of survey respondents who used Redfin in the last 3 months live in the Pacific region. This aligns with the Top-10 Redfin markets that account for 70% of its revenue: Boston, Chicago, Los Angeles, Maryland, Orange County, Portland, San Diego, San Francisco, Seattle, and Virginia.11 Because Redfin is a brokerage, we hypothesize that Redfin focused first on more on the areas with higher real estate transaction values.

Relevant Funding and M&A

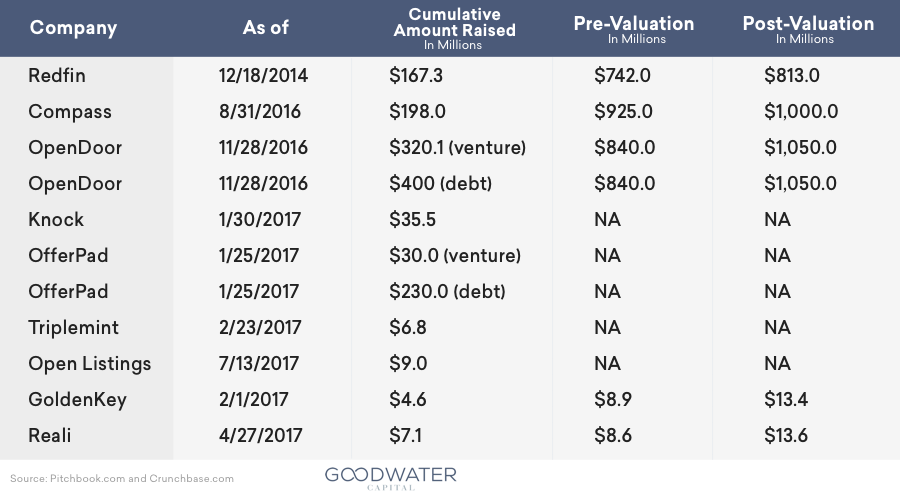

Redfin has raised $167M since inception, with the last round in December 2014 valuing the business at an estimated $813M.12 Compass, another next-generation hybrid online brokerage, has raised $198M with a latest valuation of $1B as of August 2016.13 Other companies in the hybrid online brokerage space have raised significantly less capital.

Verticalized brokerages require significant amounts of capital because their business model requires acquiring real estate inventory. OpenDoor raised $720M (both equity and debt financing) since inception and was valued at over $1B in November 2016. OfferPad has raised around $30M in venture funding and $230M in debt financing.

There have been several real estate acquisitions in the last few years. Within the US, below are the notable transactions in the sector.

- StreetEasy (August 2013): acquired for $50 million by Zillow.14

- Ziprealty (August 2014): acquired for $166 million by Realogy.15

- Realtor.com (November 2014): acquired for $950 million by News Corp.16

- Trulia (February 2015): acquired for $3.5 billion by Zillow.17

Executive Team

- Glenn Kelman (President, CEO, and Director): Prior to joining Redfin, Glenn co-founded Plumtree Software, a provider of software products for deploying Web applications, where he served as VP of Marketing and PM. Glenn holds a B.A. in English from University of California, Berkeley.

- Chris Nielsen (CFO): Prior to joining Redfin, Chris served as CFO and COO at Zappos.com, an e-commerce platform for shoes and clothing. Prior, Chris led as VP of Home & Garden, a retail business segment of Amazon.com, Inc. Chris holds a B.S. in Industrial Engineering from Stanford University and an M.B.A from the MIT Sloan School of Management.

- Bridget Frey (CTO): Prior to joining Redfin, Bridget served as Director of Analytics and Business Applications and a principal software engineer for Lithium Technologies, Inc. In the past, Bridget has also managed engineering teams at IMlogic, instant messaging security software provider, and IntrinsiQ, a chemotherapy software company. Bridget holds an A.B. in Computer Science from Harvard College.

- Scott Nagel (President of Real Estate Operations): Prior to joining Redfin, Scott served as Managing Director at LexisNexis, provider of legal, business and risk-management research services. In the past, Scott served as VP of Strategy and Client Operations at Applied Discovery, provider of legal services software. Scott holds a B.A. in Political Science from the University of Washington and a J.D. from Seattle University School of Law.

- Adam Wiener (Chief Growth Officer): Prior to joining Redfin, Adam served as Lead Program Manager in the SQL Server Division at Microsoft, Inc. Adam holds a B.S. in Symbolic Systems from Stanford University.

- RDFN S-1, at page 2.

- Realogy’s SEC Form 10-K Filing (February 24, 2017), at page 52 using RFG and NRT Combined 2016 revenues of $4.8 bilion) and RDFN S-1, at page 58.

- RDFN S-1, at page 44.

- RDFN S-1, at page 2.

- Source: Forbes (https://www.forbes.com/sites/amyfeldman/2016/11/30/home-shopping-networkers-opendoor-is-upending-the-way-americans-buy-and- sell-homes)

- RDFN S-1, at page 1.

- RDFN S-1, at page 1.

- RDFN S-1, at page 21.

- RDFN S-1, at page 60.

- RDFN S-1, at page 60.

- RDFN S-1, at page 57.

- Pitchbook.com

- Pitchbook.com

- Techcrunch (https://techcrunch.com/2013/08/19/zillow-acquires-streeteasy-for-50m-for-more-nyc-real-estate-listings-also-listing-follow-on- offering-of-2-5m-shares/)

- Source: Inman (https://www.inman.com/2014/07/15/realogy-acquiring-ziprealty-for-166-million/)

- Source: LA Times (http://www.latimes.com/business/la-fi-1001-newscorp-realtor-20141001-story.html)

- Source: Trulia (http://info.trulia.com/trulia-zillow-deal-closes)